News & Insights

The latest industry news, interviews, technologies, and resources.

.svg)

Upstix Case Study for Pre Mover

Upstix Case Study for Pre Mover: “Moving house is such a fundamental trigger point for so many suppliers. Pre Mover gives us an edge that others don’t have”

“Moving house is such a fundamental trigger point for so many suppliers. Pre Mover gives us an edge that others don’t have”

Upstix, a leading house iBuyer in the UK, provides people with a new way to sell their home. But as a disruptive start-up, the biggest challenge for COO Frederick Jones is identifying and marketing to people who are actively planning to sell their house.

Using the Pre Mover AI tool from Outra enables Upstix to not only target who is about to put their house on the market, but also to focus on the segment of those most likely to use an iBuyer.

.png)

The challenge: Identifying and engaging people actively planning to sell their houses

The most valuable consumer group in the UK are home-movers. They spend more before, during and after their move than any other consumer segment.

For Upstix to survive in a very competitive market, Frederick has to be able to maximise the return on his marketing investment by successfully targeting people who are actively planning to sell their house. “My challenge is to originate actionable leads in a very cost-effective way. We just can’t afford to spray and pray.”

On average homeowners spend £13,000 within a year of moving on expenses like renovations, furniture and electronics.

The solution: Pre Mover has a proven 1 in 4 success rate of identifying people selling their house in the next 6 months.

Precise Segmentation

Outra have trained Pre Mover to not only identify the people in the UK planning to sell their house, but also to focus on the people most likely to use an iBuyer. Pre Mover uses 2,300 data points and 130 signals to identify people who are looking for a quick sale, potentially due to probate or financial distress, and that have the type of property Upstix can sell on quickly. “Pre Mover gives us the base level of home-movers, and then we can apply various other layers on top of that around individuals in the household and the type of property, so we're able to precisely segment the type of person and specific location of houses on streets.”

No matter what segment of the home-movers your company targets, Pre Mover can be configured to find them.

Continual optimisation

A key part of the partnership between Outra and Upstix is the continual optimisation of the tool. “We do a 360 degree refresh every three months and we evaluate the success of every campaign to improve the machine learning. This segmentation analysis feeds into where we target our social media and direct mail spend, and the look-alike audience for email campaigns. It is an iterative process so we can constantly improve and retarget our marketing with Pre Mover.”

Machine learning within Pre Mover means that the longer it focuses on a segment, the more precise it gets, and so results continually improve.

Sales and marketing integration

Frederick also sees the benefits along the whole sales funnel. “It’s not just about targeting people initially, but also about how they go through sales and actually become clients. The whole sales funnel is continually fine tuned from top to bottom.”

90% of Upstix’s leads come from targeted advertising. This means that Frederick’s team isn't waiting for people to find them by chance as they search online. Upstix are proactively approaching the right people at the right time. What is more, the successful conversion rate on these leads is 12% which is four times the industry average.

“When leads come in, our sales team is spending time speaking to people who understand our service, and are in a position to sell. So we are having much more impactful conversations”.

The benefits: Evidence that your marketing is delivering return on investment

“A lot of companies promise better data analytics and more leads, but most don’t deliver”

Real estate DNA

A big factor that gives Frederick confidence in Pre Mover is that real estate is in Outra’s DNA. Outra’s founders have decades of real estate experience and a deep understanding of what data is meaningful and informative.

.png)

Fail-safe accuracy

The other big reason why Frederick believes in Pre Mover, is that there is a fail-safe way to check its accuracy. “If Pre Mover predicts a house move, say 98 Elscott Road, we can check on The Land Registry six months later, and see if that property actually has changed ownership”. This gives us a definitive score-card for Pre Mover, and a sure-fire way of optimising checking its accuracy.”

“To see the success of the model makes me feel really confident. It gives us an edge, and makes me believe the business will be a success”

The Art of Targeted Advertising with Home Mover AI

Maximise ROI with Home Mover AI's Precision Timing in Advertising

In the intricate dance of advertising, timing is not just a factor—it's the central stage. Home Mover AI has revolutionised this aspect, bringing an unprecedented level of precision to targeted advertising. By tapping into the predictive power of Home Mover data, advertisers can now reach potential customers exactly when they are most likely to make key decisions; significantly boosting the effectiveness of marketing campaigns.

Section 1: Applying Home Mover Insights Across Industries to Reinvent Marketing ROI

Elevating Marketing Strategies with Predictive Accuracy

The Home Mover product from Outra, with its advanced AI and predictive analytics, offers an innovative approach to enhancing marketing ROI. By accurately predicting when individuals are planning to move homes, this tool enables advertisers across various industries to time their campaigns to this critical decision-making phase. This precise targeting ensures that marketing messages are not just relevant, but also delivered at the most opportune moment.

Real-World Impact Across Diverse Sectors

For instance, a furniture retailer can utilise Home Mover data to identify prospective customers who are in the process of moving, offering them timely deals on home furnishings. Similarly, a telecom provider can target households moving to new areas with special broadband and TV package offers. These targeted approaches ensure higher engagement rates, thereby leading to improved conversion rates and maximised sales efficiency.

Section 2: Innovative Use Cases Across Industries that Benefit from Home Mover Insights

Versatility of Home Mover Data in Targeted Advertising

The application of Home Mover data is not limited to a single industry; its benefits span across numerous sectors. This predictive tool can be used by companies in fields ranging from home entertainment to personal finance, each leveraging data to meet their specific advertising needs.

Precision in Campaign Execution

The strength of Home Mover lies in its ability to offer high-intent consumer targeting. For instance, an insurance company can utilise this data to identify households that are relocating to new home, and might be in need of home insurance products. This level of precise targeting enables businesses to not only reach the right audience but also to do so at a time when their products are most needed, thereby significantly enhancing campaign success and ROI.

Section 3: How Home Mover Data Has Become King of Targeted Success with Predictive Marketing in the Digital Age

The Evolution of Digital Advertising

Amidst the rapidly evolving digital advertising landscape, predictive marketing has taken centre stage. The ability to forecast consumer behaviour and preferences has become increasingly vital for marketing success. Home Mover data, with its rich predictive insights, emerges as a critical asset in this new era, enabling advertisers to craft campaigns that are not just reactive, but proactively aligned with consumer needs.

Home Mover as a Cornerstone in Predictive Marketing

Home Mover's data stands out as a key player within this transformative period. It provides advertisers with a powerful lens in which to view potential customer transitions, particularly in the context of moving homes. This insight proves crucial, as a home move often triggers a series of purchasing decisions. By tapping into this data, marketers can anticipate needs and offer solutions before the consumer actively seeks them out, thereby positioning their brands strategically in the customer's journey.

Shaping the Future of Marketing Strategies

The predictive power of Home Mover data is reshaping how marketing strategies are formulated. Instead of a scattergun approach, advertisers can now employ precise, data-driven strategies to target consumers. This shift not only improves the relevance and effectiveness of advertising campaigns but also enhances the overall consumer experience, as messages and offers are more likely to align with the consumer’s current life stage and needs.

Section 4: Anticipating Consumer Behaviour By Leveraging Data for Effective Campaigns

Harnessing Predictive Insights for Timely Engagement

The core strength of Home Mover data resides in its ability to anticipate consumer behaviour with remarkable accuracy. This predictive insight is invaluable for advertisers aiming to engage with their audience at the most opportune moments. Understanding when consumers are likely to make significant life changes, such as moving homes, allows for the crafting of campaigns that are not only relevant but also exceptionally timely.

Strategic Campaign Planning with Home Mover Data

By leveraging Home Mover insights, advertisers can strategically plan their campaigns to coincide with these key decision-making periods in consumers’ lives. This could involve targeting individuals with offers for home-related services and products, or providing timely information that assists them during the moving process. Such targeted and well-timed advertising not only improves campaign performance, but also enhances customer experience, leading to stronger brand loyalty and long-term engagement.

Section 5: Future-Proofing Marketing Strategies with Home Mover AI

Adapting to a Changing Marketing Landscape

As the marketing world continues to evolve, staying ahead of the curve becomes increasingly important. Home Mover AI is an essential tool in this respect, offering a forward-looking approach to predictive marketing. By understanding and anticipating the shifts in consumer lifestyle and behaviour, advertisers can future-proof their strategies, ensuring relevance and impact in a consistently evolving market.

The Continuous Evolution of Targeted Advertising

The integration of AI and data analytics in marketing is not a fleeting trend but a fundamental shift. Home Mover data is at the forefront of this shift, continually refining the way advertisers approach campaign planning and execution. Its role in the future of marketing is not merely about targeting the right audience but also about fostering a more intuitive and responsive advertising ecosystem.

Conclusion

The art of targeted advertising in the digital age has been significantly enhanced by the advent of predictive tools like Home Mover AI. This innovative approach has revolutionised the way advertisers plan and execute their campaigns, ensuring that they reach consumers precisely when they are most receptive. The predictive power of Home Mover data has not only redefined marketing ROI but also established a new standard for customer engagement and satisfaction. As the marketing landscape continues to evolve,the strategic use of such AI-driven insights will undoubtedly play a pivotal role in shaping the future of targeted advertising, making timing not just a factor, but the essence of successful marketing strategies.

Predictive Home Mover Marketing How Any Industry Can Benefit

Discover the power of predictive Home Mover marketing to boost ROI across diverse sectors

In the fast-evolving world of marketing, the ability to anticipate consumer needs and behaviours is a coveted advantage. Enter the realm of predictive marketing, a technique that leverages data to foresee consumer actions. At the forefront of this revolution is Home Mover data, a tool that, while closely associated with real estate, holds untapped potential for a myriad of industries. This article delves into the versatility of Home Mover data, exploring how it can serve as a linchpin in understanding consumer intentions and reshaping marketing strategies across various sectors.

Section 1: Anticipating Consumer Behaviour by Leveraging Data for Effective Campaigns

The Importance of Consumer Insights

In today’s data-driven marketing landscape, understanding consumer behaviour is not just beneficial; it's essential. Home Mover data provides a window into the minds of consumers before they make significant life changes. This home mover information is invaluable, as it gives marketers in any industry a head start in tailoring their strategies to meet the evolving needs of their audience.

Shaping Advertising Strategies

The ability to anticipate when a consumer is planning to move can revolutionise advertising campaigns. For instance, retailers can target pre-movers with promotions on home furnishings, while automotive companies might highlight family-friendly vehicles. This foresight allows for a more strategic, targeted approach, ensuring that marketing efforts are not only seen, but are also relevant and compelling.

Section 2: Personalised Marketing for Any Business by Crafting Tailored Ads with Home Mover Data

The Era of Personalisation in Advertising

Personalised marketing has become the cornerstone of successful advertising campaigns. In an age where consumers are bombarded with generic advertisements, the ability to stand out with tailored messaging is invaluable. Home Mover presents a unique opportunity to personalise advertising efforts based on imminent life changes.

Creating Customised Ad Experiences

By leveraging Home Mover's predictive data, businesses across various industries can craft ads that directly address the needs and preferences of home movers. For example, a telecommunications company can offer special broadband packages to individuals moving to a new area, or a pet supply company can target pet owners moving to a property with more outdoor space. Such customisation not only enhances the relevance of the ads but also significantly boosts consumer engagement.

Section 3: Applying Home Mover Insights Across Industries To Reinvent Marketing ROI

Transformative Impact on Marketing Returns

The utilisation of Home Mover data has been shown to revolutionise the return on investment (ROI) in marketing campaigns across diverse sectors. By targeting consumers at a time when they are most receptive to certain products and services, businesses can achieve higher conversion rates and better returns on their marketing spend.

Case Studies and Examples

Consider the case of a home improvement retailer that utilised Home Mover data to target individuals planning to move. By offering tailored promotions and services, the retailer witnessed a significant uptick in sales and customer engagement. Similarly, a financial services company leveraged this data to offer home insurance and mortgage products to potential movers, resulting in a higher uptick of their services and an improved ROI.

Conclusion

Home Mover data transcends its traditional real estate confines, proving to be a versatile and powerful tool in the realm of predictive marketing. Its ability to provide insights into consumer behaviour and intentions before a major life event like moving house, is invaluable for marketers across various industries. By enabling personalised advertising and enhancing marketing ROI, this data not only meets the current demands of a data-driven advertising world but also sets the stage for future innovation. As businesses continue to seek more targeted and effective marketing strategies, the role of predictive analytics, especially in the form of tools like Home Mover, is set to become increasingly pivotal.

The Home Mover Shield To Safeguard Revenue in Insurance

Home Mover lifecycle insights and AI is crucial to the insurtech stack to safeguard revenue and customer value

In the fiercely competitive landscape of the insurance industry, the ability to protect and grow revenue streams is paramount. Senior decision-makers and C-suite executives are constantly on the lookout for innovative strategies that align with this objective. Understanding the Home Mover lifecycle through the power of data and AI offer a unique advantage by predicting customer household moves, thereby enabling insurers to make timely strategic adjustments. This foresight not only retains revenue but also minimises potential disruptions in the customer journey.

The Home Mover Strategy for Insurers To Maximise Customer Lifetime Value

The Essence of Customer Lifetime Value

In the realm of insurance, understanding and maximising customer lifetime value (CLV) is crucial for sustained success. CLV represents the total worth of a customer to a business over the entirety of their relationship. For insurers, this means not just selling a policy, but nurturing a long-term relationship that evolves with the customer’s changing needs.

Leveraging Home Mover Insights

Gaining deep insights through data and technology into when and why customers are likely to move homes, insurers can tailor their services to accompany customers through different life stages. Whether it’s adjusting coverage when a customer moves to a bigger home or offering additional policies relevant to new life circumstances, these targeted services significantly enhance CLV.

Unleashing Home Mover Data for Diverse Insurance Product Cross-Selling Power

The Strategic Advantage of Cross-Selling

In insurance, cross-selling is not merely a sales tactic; it's a strategic approach to deepen customer relationships and enhance revenue. By offering customers additional, relevant products, insurers can address a broader range of customer needs, reinforcing their role as comprehensive service providers.

Utilising Home Mover Insights for Effective Cross-Selling

Predicting when a customer is about to move through home mover lifecycle data and AI plays a crucial role here. When a customer is in the process of moving homes, their insurance needs invariably change. This transitional phase presents an opportune moment for insurers to cross-sell various insurance products - from property insurance to contents insurance. By aligning these offerings with the specific circumstances of the home move, insurers ensure relevance, which is key to successful cross-selling.

Tailoring Upsell Strategies Using Home Mover Predictive Insights

Upselling as a Revenue Growth Lever

Upselling, the practice of encouraging customers to purchase more coverage adding products, upgrades, or other add-ons, is a powerful tool for revenue growth in insurance. It goes beyond mere transactional sales; it's about providing customers with value-added services that genuinely enhance their coverage.

The Role of Predictive Insights in Upselling

Home Mover lifecycle data insights and the power of AI is becoming invaluable within the insurtech stack. These insights enable insurers to identify moments when customers might be most receptive to upselling. For instance, if the data indicates a customer is moving to a high-value property, it’s an opportune time to suggest premium insurance packages or additional coverage options. Tailoring upselling strategies in this manner ensures that offerings are not only timely but also highly relevant to the customer's current needs and lifestyle changes.

Retention Reinvented With Home Mover Insights To Secure Insurance Customer Loyalty

Enhancing Retention through Personalised Interactions

In insurance, retaining a customer is often more cost-effective than acquiring a new one. Home Mover insights offer a robust solution to the retention challenge by enabling highly personalised customer interactions. By understanding when customers are likely to move, insurers can proactively offer relevant services and support, demonstrating attentiveness to the customer's life changes.

Building Loyalty with Continuous Value Delivery

Loyalty in the insurance sector is fostered not just through competitive pricing but, more importantly, through continuous value delivery. Home Mover insights enable insurers to stay one step ahead, anticipating customer needs and offering solutions before the customer even recognises the need themselves. This proactive approach builds a strong sense of trust and reliability, essential components of customer loyalty.

Future-Proofing Insurance Revenue with AI

Anticipating Customer Behaviour Shifts with AI

The future of insurance revenue lies in the ability to anticipate and adapt to customer behaviour shifts. AI and predictive analytics, as exemplified by Home Mover, are key to this adaptability. By harnessing these insights, insurers can not only protect existing revenue streams but also identify new growth opportunities.

Adapting Strategies for Sustained Growth

The dynamic nature of AI-driven insights allows insurance companies to continuously refine their strategies in line with evolving customer preferences and market conditions. This agility is crucial for not just surviving but thriving in the rapidly changing insurance landscape. Home Mover lifecycle insights combined with AI and technology represents a significant step in this direction, offering a tangible way for insurers to future-proof their revenue streams.

Empowering Modern Insurers to Safeguard Revenue and Customer Value

Outra's Home Mover emerges as a pivotal tool in the strategic arsenal of modern insurance companies, particularly in the quest to safeguard and grow revenue. By maximising customer lifetime value, enabling effective cross-selling and upselling, and enhancing customer retention, this tool represents a comprehensive solution to several key challenges facing insurers today. Moreover, the integration of AI and predictive analytics signals a broader shift in the industry towards more adaptive, customer-centric models. As senior decision-makers and C-suite executives navigate this evolving landscape, tools like Home Mover are not just advantageous; they are essential for future-proofing revenue in a world where understanding and anticipating customer needs is paramount.

Elevating Customer Experience for Insurance in 2024

The journey towards an AI-driven insurance future, led by innovations like the Home Mover, is not just imminent; it is already underway.

In an era where customer experience (CX) dictates the rise or fall of companies, the insurance sector is not immune to these winds of change. Traditionally viewed as a necessity rather than a choice, insurance services are now undergoing a radical transformation, primarily driven by personalisation and predictive analytics to redefine customer engagement through cutting-edge AI capabilities.

Section 1: Customer-Centric Insurance With Home Mover Personalisation

The Importance of Personalisation

In today's digital age, personalisation is not just a buzzword but a business imperative. Customers expect services that are not only efficient but also tailored to their unique needs and life situations. By leveraging deep insights into household moves, innovative technology and AI enables insurance companies to craft highly personalised experiences that resonate with each individual customer.

Facilitating Personalisation with Insights

Harnessing the power of big data and AI to predict when individuals are likely to move home allows elevated customer experiences within the insurance sector. This predictive capability allows insurance providers to offer tailored insurance solutions at just the right moment. Whether it’s updating a homeowner's policy or suggesting new coverage options, these timely interventions foster a sense of understanding and care, crucial for building long-term customer relationships.

Section 2: Insurance Evolution: Home Mover Insights and the Life Insurance Revolution

Transforming Traditional Life Insurance Offerings

Life insurance, a cornerstone of long-term financial planning, has traditionally been a static offering, often disconnected from the dynamic nature of customers' lives. By integrating predictive insights into customer movements, life insurance providers can now adapt their offerings to align seamlessly with the evolving life stages and needs of their clientele. A seismic shift to the insurtech landscape to better understand consumer needs with a more dynamic product offering.

The Power of Predictive Personalisation

Imagine a scenario where an insurance provider can anticipate a customer's move to a larger home, possibly indicating a growing family. Armed with this insight, the provider can proactively offer enhanced life insurance coverage or family plans, resonating perfectly with the customer’s current life situation. This level of personalisation, powered by predictive analytics, not only delights customers but also positions the insurance provider as a proactive, caring partner in the customer's life journey.

Benefits of Timely and Tailored Solutions

The benefits of this approach are manifold. Customers receive life insurance solutions that feel personalised, timely, and relevant, significantly enhancing their satisfaction and trust in the provider. For insurance companies, this translates into deeper customer engagement, increased policy uptake, and a competitive edge in a market that is increasingly customer centric.

Section 3: Retention Reinvented: How Home Mover Insights Secure Insurance Customer Loyalty

Addressing Customer Retention Challenges

In the competitive landscape of the insurance industry, retaining customers is as crucial as acquiring new ones. Traditional retention strategies often fall short in understanding and addressing the evolving needs of customers. This is where Home Mover insights become a game-changer.

Personalised Interactions and Continuous Value Delivery

By leveraging data on imminent household moves, insurance providers can tailor their communications and offerings to meet the changing needs of their customers. Such personalised interactions are not just about selling more; they're about delivering continuous value, showing customers that their insurance provider understands and adapts to their life changes. This approach cultivates a sense of loyalty and trust, making customers more likely to stay with their provider for the long haul.

Impact on Customer Loyalty

The impact of using Home Mover insights can be significant. Customers who experience this level of personalisation and attentiveness are more likely to view their insurance provider as a trusted advisor, not just a service provider. This shift in perception is critical for long-term loyalty, as satisfied customers are not only more likely to renew their policies but also to recommend the provider to others, thus driving both retention and new customer acquisition.

Section 4: Redefining Insurance Revenue With Home Mover AI

Revolutionising Traditional Revenue Models

The introduction of predictive analytics through tools like Outra's Home Mover is not just transforming customer experience; it's also redefining how revenue is generated and protected in the insurance sector. Traditional models often rely on static customer profiles, leading to missed opportunities and a reactive approach to customer life changes. With predictive insights, insurance companies can shift to a more dynamic, proactive model.

Optimising Offerings for Revenue Protection and Growth

The predictive capabilities of the Home Mover product allow insurance companies to anticipate and respond to key life events of customers, such as moving to a new home. This foresight enables the optimisation of insurance offerings to suit these new circumstances, thereby not only retaining existing customers but also increasing the potential for upselling and cross-selling relevant insurance products. Such tailored solutions are more likely to be embraced by customers, leading to enhanced satisfaction and, consequently, revenue growth.

The Future of Insurance Revenue with AI

As the insurance industry continues to evolve, the integration of AI and predictive analytics heralds a new era of revenue models. These models are customer-centric, responsive, and agile, aligning closely with customers' real-time needs and preferences. The Home Mover product exemplifies this shift, presenting a promising future where insurance revenue is not just about policy sales, but about building and maintaining enduring, value-driven customer relationships.

Conclusion - Home Mover Lifecycle AI is a beacon of innovation for insurance

Understanding the predictive Home Mover lifecycle with AI is a beacon of innovation in the insurance sector, significantly elevating the customer experience. From personalising insurance offerings to revolutionising life insurance and reinventing customer retention strategies, the predictive insights provided by this tool are reshaping the industry. Moreover, the impact of these insights extends beyond customer satisfaction, playing a pivotal role in transforming revenue models and securing long-term financial success for insurance companies.

As we look to the future, the integration of AI and predictive analytics in insurance promises not just enhanced business outcomes but also a more intuitive, responsive, and customer-centric industry. The question now is not whether insurance companies will adopt such technologies, but how quickly they can adapt to leverage these advancements to their fullest potential. The journey towards an AI-driven insurance future, led by innovations like the Home Mover, is not just imminent; it is already underway.

2024 Real Estate Goals - Proptech and Data at Your Service

Keeping ahead of proptech advances is essential for any early-career exec in establishing themself as a contemporary property professional

Residential property moves into 2024 with determination, yet still not without some measure of nerves. The uncertainties the market has shown through 2023 are certainly not yet resolved, and it’s against this backdrop that professionals across the sector must shape their strategies for achieving meaningful goals in 2024.

Today, proptech is the most ubiquitous of industry terms, raising its head in almost every conversation. As the power of proptech tools offers all property professionals so much potential for achieving their targets and objectives, it’s worth taking a moment to recount where, precisely, we are on the proptech journey.

First appearing well over thirty years ago, proptech – property technology – refers to the application of technology within the real estate business. In its first iteration, up until around 2000, this involved little more than the use of spreadsheets for managing listings and client and financial data.

The second stage of the proptech revolution started in the dotcom boom of the late nineties, and transformed the sector by providing customers, by then all with high speed internet connections, with tools for searching listings online.

The third stage, in which we now find ourselves, is the most exciting of all. With the aid of innovative tools, software and platforms it is revolutionising traditional agency methodologies and practices at both a strategic and executive level, through the analysis of high volumes of consumer and market data, and the implementation of strategies built around insights obtained from that data. This isn’t merely a further incremental addition to the business of estate agency. It's a fundamental shift that redefines the way professionals engage with the sector.

So what does this mean for the rising stars and junior professionals now navigating the complexities of the industry? The answer lies in its transformative potential. Proptech offers today’s generation of property professionals tools and insights which are essential for elevating their performance by providing a lens through which to analyse market trends, consumer behaviours and property data with unprecedented clarity.

This, in turn, enables them to make informed decisions, forecast market movements, and steal a march on competitors (as well as on colleagues) by drawing inferences others may not have made, and responding swiftly to evolving demands. For anyone in the early years of their career, this kind of technology, which younger professionals reared on the use of data in all kinds of contexts may find far easier to integrate into their work than their seniors, offers a launchpad from which to succeed and thrive amidst the changing tide. Using theses kinds of advanced analytics, automation tools and collaborative platforms, younger professionals should be able to leapfrog traditional career barriers, and supercharge their trajectory within the industry.

The power of leveraging data in real estate

It would be a grave misjudgement at this point to view property insights driven by analytics as a ‘coming’ wave. While the applications and impacts seem certain to proliferate in the next few years, practical use of the tools is very much ‘here and now’.

Fred Jones, formerly Managing Director of Uber, is COO at ‘instant’ home offer platform, Upstix. The company uses proptech data analytics innovator Outra’s Pre-Mover platform to identify the specific properties and buyers it wishes to target.

“We get an amazing amount of data through Pre-Mover”, Jones explains. “This includes demographic type, propensity to sell and property type, all in different regions within the UK. It's just brilliant. In the first three months of using this tooling, we increased our conversion by 3.5x.”

In an era in which so many sectors are already ruled by data-driven decision-making, this is no mere trend. It’s fast becoming the linchpin for real-estate success, having transformed from an advantage to a necessity for professionals aiming to achieve challenging industry goals.

So why does this hold so much significance? The answer lies in the strategic advantages it makes available. Until relatively recently real estate, as a business, depended on instinct and experience. Today, it is increasingly driven by empirical insights and predictive analytics. The capacity to leverage comprehensive data repositories means professionals can navigate the market with precision, foresight, and unparalleled efficiency.

The value of data extends far beyond mere statistics. It embodies a treasure trove of patterns, trends, and invaluable insights which, when deciphered, provide a blueprint for success. It puts the pulse of consumer behaviour, the whole picture on market fluctuations, and the ebb and flow of property dynamics all at the fingertips of individual agents and strategic managers able to harness them wisely.

Like Fred Jones, Robin Patterson, the former owner of Sotheby's Realty and now Founder of Upstix, is evangelical in his belief in the data analytics and insights provided to his firm by Outra’s product, Pre-Mover.

“Any real estate business looking for data on either their buyer or seller… Outra is able to provide it, which allows them to be very focused on their core markets,” says Patterson. “It allowed us to improve our buy boxes, lead generation and pre-seller records, enabling our pre-move model to be focused and target those people looking to move.”

The secret, of course, lies not only in the quality of the data (Outra’s Pre-Mover monitors 30.8m UK households, tracking 2,300 attributes per record via more than 60 quality data sources), but also in the tech used to leverage it. From advanced analytics and machine learning algorithms to intuitive platforms and automation tools, this is what amplifies the capability to extract the actionable insights that enable property professionals to anticipate market movements, identify untapped opportunities and tailor strategies with pinpoint accuracy.

Whether seasoned veterans or emerging talents, it’s this marriage of data with exceptional technology that transforms all of those records and attributes into strategic intelligence, and empowers property pros to stay ahead in a landscape defined by its dynamism and competitive edge.

Trends and Innovations in Proptech

The kind of predictive analytics employed by Upstix through Outra’s Pre-Mover product is one of the key aspects of modern proptech, enabling executives and managers working in UK residential real estate to forecast future trends, behaviours and outcomes, and so make better decisions, optimise performance and gain valuable competitive advantage.

Embracing these tools, and taking ownership of them within the organisation, offers more recent recruits into the real estate business a clear roadmap not only to success against 2024 business goals, but to accelerated career profile and industry success. So, moving into 2024, what are the most important trends and innovations in this kind of proptech?

- In the area of demand and supply forecasting, predictive analytics can help real estate professionals to understand the current and future demand and supply of residential properties in different locations, segments, and price ranges. This can help them to identify opportunities, adjust pricing, and allocate resources accordingly.

- In customer segmentation and personalisation, products like Outra’s Pre-Mover can help to segment and target customers based on their preferences, behaviours, and needs. This can help agents to tailor marketing, communication, and service strategies to each customer segment and deliver a personalised and engaging customer experience.

- Predictive analytics can also help real estate professionals with valuation and appraisal, making it possible to estimate the value of residential properties based on factors such as location, size, condition, amenities, and market trends. This can help with appraising properties accurately, negotiating deals effectively, and avoiding overpaying or underpricing.

- Data analytics can also be used to optimise an agency’s portfolio of residential properties by identifying the best mix of assets, markets, and strategies. This can help it to maximise its returns, diversify its risks and align its portfolio with its strategic goals and objectives.

Pre-Mover identify the earlier discovery of hyper-targeted leads; identification of high-intent audiences; optimisation of marketing spend; increased ROI through reduced cost per lead; competitive advantage through being able to approach high-intent customers sooner; increased revenue from increased access to highly motivated vendors; increased market share; and accelerated growth of market share for new branches as key benefits of their product. Addressing, as this does, almost every essential metric of residential agency performance, it’s impossible to take issue with the company’s founder, Giles Mackay, when he argues that, “In the dynamic landscape of real estate, harnessing the power of data is not just a strategy; it's a necessity. Early identification of motivated sellers is a prime example of how data can be the catalyst for exceeding sales targets."

Hitting performance and career goals for 2024

For any junior professional working in residential real estate and determined to surpass annual goals, position themselves ahead of peers and add to their achievements in 2024, the signposts could scarcely be clearer.

First, proptech is now the key transformative actor in the reinvention of residential sales as an industry, and by actively participating in its adoption and application in the organisation, an executive can position her/himself both at the head of annual performance tables, and in pole position for career fast-tracking.

Next, sector data, data analytics and the insights that these can provide can boost both your personal and company performance in all areas of the business.

Lastly, advances in proptech are continuous. Keeping ahead of these is essential for any early-career exec in establishing themself as a contemporary property professional whose success is attributable primarily to their facility with data and data tools. The websites and product downloads of proptech leaders (such as Pre-Mover creator Outra) provide a valuable starting point for expanding knowledge of the landscape and laying the foundations for making 2024 a true breakthrough year.

Unlocking Real Estate Success With Data-driven Insights To Propel You Past Your 2024 Targets

Data-driven insights can no longer be viewed as a ‘nice to have’ competitive advantage.

Bullishness and determination count for a great deal in sales, and nowhere more so than in property sales. They cannot, however, do much to counter the uncertainty the market that will carry over from 2023. Sellers will enter 2024 continuing to weigh lower valuations than they’d like against the prospect of increasingly lower purchase prices and mortgage rates that may begin to edge down again soon – unless they don’t!

In a market with this level of instability, beating sales goals calls for a far more dependable, which means data driven, strategy.

"In the dynamic landscape of real estate”, argues Giles Mackay, founder of real estate data analytics leaders, Outra, “harnessing the power of data is not just a strategy; it's a necessity. Early identification of motivated sellers is a prime example of how data can be the catalyst for exceeding sales targets."

How can data help real estate professionals meet and exceed sales targets?

Mr Mackay’s assertion is not unjustified. Data can empower anyone involved in residential sales, by providing actionable insights that help optimise effort, streamline processes and which will, ultimately, lead to beating of sales targets.

With effective predictive analytics, anyone in residential sales has comprehensive insights into market trends, buyer behaviour, and seller patterns at their disposal. By understanding these trends, they can anticipate market movements, adjust strategies accordingly, and target their efforts more effectively.

Leveraging data then allows for precise targeting of potential clients. By analysing demographics, preferences, and past behaviours, it becomes possible to identify and focus on the most promising leads, optimising use of both time and effort. By using predictive analytics to forecast when properties are likely to be listed for sale, sales teams can engage proactively with sellers, gaining competitive edge and increasing the likelihood of closing listings.

Data-driven insights also offer a solid foundation for making informed decisions around sales strategy. Whether on pricing or geographic targeting, for example, comprehensive data combined with robust analytics enables calls to be made with vastly improved confidence. In addition, at individual listing level, data can help build stronger client relationships by providing insights into client needs and preferences. This allows agency sales teams to deliver more personalised advice, guidance and service, fostering trust and increasing loyalty.

“The real Focus for everybody in the real estate space, “ says Fred Jones , COO of ‘quick sale’ cash buyer, Upstix, “is to get sellers before anybody else gets there. If we can do that then we've revolutionized the way anybody runs the real estate space.”

How identifying motivated sellers before they list improved performance.

Being able to identify motivated sellers before they list their properties delivers substantial advantages in achieving sales targets. Connecting with sellers identified as highly likely to list before their property hits the market lets you establish rapport and build relationships. This increases the likelihood of securing the listing, giving a head start in the sales process. It also, of course, reduces competition from other agents. By being the first point of contact, you have a better chance to negotiate terms, potentially agreeing more favourable conditions for both you and the seller.

Data analytics also offers the potential to offer upcoming sellers the option of an off-market deal. This means you may be able to offer a solution to specific needs or wishes, such as privacy concerns or the desire for a quick completion, and potentially expedite their sale.

With the insights provided by high grade analytics making it possible to understand a seller's motivation early on, sales teams also have an improved basis on which to tailor sales strategies. Whether this is by highlighting certain property features, offering more flexible terms, or addressing a specific concern a seller may have, the data insights make it possible to craft personalised approaches which maximise the chances of landing the instruction and achieving a successful sale.

Building a relationship with a seller before they list their property may also lead to a higher closing rate, through being able to better understand seller expectations, manage negotiations, and guide the sales process more effectively.

With HMRC National Statistics recording a provisional, non-seasonally adjusted, estimate of the number of UK residential transactions in September 2023 down 19% on September 2022 (and down 2% on August 2023), advantages of the kind gained through identifying motivated sellers before they list could step any sales team closer to not only achieving, but impressively outperforming, their 2024 targets.

The best data and analytics tools to help you pass 2024 targets.

Proptech as a sector is booming, but while platforms aimed directly at buyers and sellers proliferate, the market for serious data and analytics designed specifically to help agents identify sellers ahead of listing is dominated by Outra’s ground-breaking product, Pre-Mover.

“In all my years involved in residential development and estate agency”, says Dominic Grace, former Head of London residential Development at Savills, “I've never seen anything as phenomenal, in terms of its power, as the Outra platform. It gives you lots of information at a really granular level… so it means you can run your whole business much more efficiently and effectively.”

Pre-Mover tracks more than 2,300 attributes each on 30.8m UK households, amounting to 75 billion data points at property level. According to Outra’s Chief Data and Technology Officer, Peter Jackson, “We make 900,000 predictions every month; they've not even listed their house yet and we're predicting when they're going to list. That's quite remarkable performance.”

Upstix’s Fred Jones agrees. “The UK housing market is hugely volatile and has changed massively over the last 12 months alone. The Outra data helps us be agile and adapt our marketing strategies to respond to that. It's allowed us to be on the front foot and capture new leads rather than being reactive.”

No longer ‘Nice to have’. ‘Must have’ in 2024.

It would be foolish to imagine 2024 won’t harbour significant challenges for the residential sector, compounded by those lingering market uncertainties. Against this unpredictability, however, data stands out as the key driver for success. Leveraging data-driven insights has become not only ‘advantageous’, but essential for exceeding sales targets.

By understanding market trends and buyer behaviours, and anticipating seller patterns, directors, area leaders and managers in firms of any size can gain a comprehensive understanding of the landscape and use this to recalibrate strategies, precisely target potential clients, and engage proactively with prospective sellers before their properties hit the market.

It is this last benefit, the ability to identify motivated sellers before their official listing, that is the real game-changer. Establishing early relationships opens doors for negotiations, reduces competition, and allows for tailored sales approaches that really impress and win over sellers.

As 2024 approaches, the use of data-driven insights can no longer be viewed as a ‘nice to have’ competitive advantage. It’s now the linchpin for success; the single most decisive factor in empowering you to not just meet, but to significantly exceed, 2024 targets.

A Data Advantage To Navigate Real Estate Volatility

Data analytics promises bold and ambitious real estate management teams a level of disruptive and transformative power

Leadership brings challenges. For anyone guiding the fortunes of a business of any scale, these challenges go with the territory. Indeed, many would say these are the territory.

While every commercial sector has its own issues to wrestle with, for anyone leading a UK residential real estate business at this time, the hurdles to be overcome (and, on the flipside, opportunities to be embraced) arise largely from the uncertainty against which the sector finds itself operating.

In the words of former Foxton’s CEO, Nic Budden, "The UK residential estate agency market is one of the most competitive and dynamic in the world, but it is also one of the most challenging and complex. We have to deal with the fluctuations and uncertainties of the housing market, the evolving preferences and behaviours of our customers, and the increasing competition and regulation in the industry. We have to be agile and innovative to stay ahead of the curve and differentiate ourselves from the crowd.” The accuracy of tis view has only been compounded by further economic turbulence.

Staying ahead of the crowd, as Mr Budden observed, really is the key issue. In a heavily populated market, how can real estate businesses develop strategies capable of securing real market advantage, when borrowing rates are high, buyers are nervous and hesitant, sellers are uncertain, the economy is sluggish and policy from the Bank and Government must be viewed as ‘continuously subject to change’?

Data analytics, real estate and a glimpse into the future

In the age of sophisticated data science and Artificial Intelligence tools, the answer seems certain to lie in innovative and timely use of analytics.

Think of the advantage to be gained at every level of the business, from operational and budgetary consideration at local office level, to organisation-wide forecasting and planning, were residential agency businesses to exploit relevant consumer and market data on a continuous basis.

In what ways could AI-driven data analytics of this kind give agents ready to embrace their forensic power and invaluable insights a competitive edge?

Fed with extensive and expertly defined data points and signals, data analytics could provide a tactical commercial weapon of a kind never before seen in real estate. Able to analyse market trends, consumer behaviour and economic indicators in myriad ways, agency leaders would be able to identify emerging market patterns, prioritise areas in which listings were about to blossom or to slow or, at a granular level, predict accurately, months in advance, when particular properties were likely to list.

At an organisational level, consistent use of data analytics in managing the business could provide estate agents with the ‘crystal ball’ of their dreams, enabling informed decisions, insight-driven business planning and early moves to obtain instructions, and providing the keen competitive edge needed to cut through the uncertainties of the market and outpace competitors.

The advantages for agents of identifying listings ahead of time

Accurate and reliable foresight into future listings could provide strategic advantage for real estate businesses in numerous ways. Early access to information about properties coming onto the market would enable agents to engage proactively with potential sellers, reaching out to offer their expertise and services before the property lists. An approach of this kind not only demonstrates a proactive operation, but positions the agent as a dependable professional partner.

Agencies able to identify soon-to-list properties early would also lay claim to the opportunity to secure the listing exclusively, gaining greater control over the marketing process and allowing for a more tailored and focused strategy to maximise a property's visibility. Similarly, with data-driven ability to analyse comparable properties and market trends, agencies could take a more authoritative position in helping sellers set competitive and realistic prices. As well-informed pricing enhances the chances of a successful transaction, this stands to minimise the time properties spend on the market.

There would be further advantages to be gained, too. In property marketing terms, amed with early visibility of upcoming listings across an area, agents would enhance their ability to optimise sale price for their clients, advising on when precisely to release a property onto the market to maximise its value. Similarly, by identifying properties before they enter the market and engaging early with vendors, agents would be able to streamline the transaction processes, preparing documentation, conducting pre-listing inspections, and addressing potential issues ahead of actual listing. This would again reduce the time the property spends on the market, creating a smoother sale process for all parties.

With the ability to predict upcoming property listings, agencies could become more proactive market leaders, able to control deals and run even the largest chain with greater precision and, as a result, enhanced success.

How early, data-driven insights show the way through uncertain economic times

By now, most real estate agency management teams have come to terms with the lingering uncertainty in the landscape. It’s ‘the way it is’. But while it’s a far from ideal environment in which to try to solidify success, managements equipped with powerful, AI-driven data analytics tools could gain high value wins.

Underpinned by the right dataset, a robust real estate tool could facilitate accurate forecasting of economic shifts by analysing predictive indicators such as employment rates, inflation and interest rates. Armed with these insights, managements would be able to anticipate how changes in the broader economy might impact the housing market, allowing them to adjust strategies on pricing, marketing or investment recommendations, accordingly.

Reaching beyond raw economic data, an effective tool might tap into sentiment analysis of market participants, letting agency teams observe shifts in consumer confidence and adjust approaches accordingly. For example, with indications of positive sentiment returning, an agency team might consider it a good time to turn up marketing efforts, while negative sentiment might advise greater caution.

Inevitably, economic uncertainty gives rise to trends and shifts in consumer behaviour. Able to analyse a myriad of data points, however, real estate businesses could observe emerging trends such as shifts in housing preferences, demand for specific amenities, or changes in preferred locations, all before these became widely apparent. Businesses with access to these insights would then be able to position themselves ahead of the curve, aligning their offerings with evolving consumer preferences.

For every business in the sector, there is also the clear need to assess and mitigate the new and increased risks inherent to transactions in times of uncertainty. Through analysis of historical data and market trends, powerful real estate tools will help agency managements identify the potential for, say, market downturns or fluctuations in values. This knowledge would make it possible for leaders to develop contingency plans and advise clients accordingly, greatly enhancing resilience.

In a market in which economic conditions can vary significantly at regional and micro-market levels, granular analysis also has the potential to help teams leading chains operating across larger areas to understand the nuances within different locales. Localised insight of this kind could prove invaluable in tailoring strategies to specific regions, optimising marketing efforts, or capitalising on opportunities that may be unique to certain areas.

Outra’s Pre Mover analytics management leads the way for real estate businesses

The application of powerful data analytics to residential real estate is a paradigm shift that can redefine success in the industry for everyone from single-office agencies through to the largest, nationwide chains.

Innovation in the space is led by Outra’s disruptive ‘Pre Mover’ product. Observing over 30 million UK households with more than 2,300 data points and 130 signals on each, Pre Mover generates highly accurate predictions about properties which are soon to be listed. It integrates analysis of real world events, such as residential sales and rental data, with a broad array of household insights, demographic data and other influencing factors to accurately predict households planning to list as far as six months in advance.

Decision time for agency leadership.

Data analytics promises bold and ambitious real estate management teams a level of disruptive and transformative power similar to those obtained in comparable sectors by organisations willing to embrace early and remodel operations and strategies around its impactful insights.

While the market maintains its current unpredictability, the consideration for all management teams should be the risk of being left for dead by competitors taking this opportunity to re-engineer their strategies and approaches around potent, AI-driven data science.

Work From Home Trends and the Race for Space

Impact of remote work on housing

In early 2020, overnight working from home (WFH) became widespread across the globe. As lockdowns have ended in the UK, we have embraced ‘the new normal’ with hybrid working models more common than ever. However, for some, the weekly commute has returned. This change in working behaviour across the UK has, over the past 2 years, dramatically impacted house prices.

With such disparity between working behaviours, Outra’s data science team has sort to identify who are these hybrid or remote workers, and how this is influencing the UK’s housing market. By analysing commuting data, we have looked to identify where the resulting ‘race for space’ is occurring. To start to understand Outra used data from a variety of sources, modelled to provide insight and identify trends, including;

- passenger data for the 40 UK stations with themost marked difference in passenger numbers - the 20 highest and the 20 lowest.

- we identified suburban stations with the highest and lowest change in entry and exit volumes as a proxy for WFH.

- the numbers of people who commute to work using the Office of Road and Rail information for the 12 months ending in March 2021.

Pre and post lockdown trends

In locations where there were minimal increases in house prices, compared to the wider UK trend, we identified 3 key factors. Where these were present, homes near these back-to-work stations, prices only rose by 8.7%.

- Train stations largely located in and around London, where properties are higher in value. Occupants are more likely to work full time, travelling to and from the office.

- Higher number of flats and apartments. Fewer bedrooms compared to more central properties, meaning occupants are less likely to have access to adequate WFH space.

- Property occupants near train and bus stations are more likely to be in managerial roles. Increased seniority requires a more regular presence in the office — resulting in more frequent commuting.

Where we are seeing the ‘race for space’, is where people in the inner cities sought to transition to WFH locations, which in turn has fuelled the UK’s property price growth. Property values near WFH stations have increased by 13.5%, outpacing average country-wide growth since 2020.

- Local properties are more often owner-occupied and bigger in size, giving less incentive to commute.

- Property occupants living far away from their offices and nearest stations are more likely to work from home.

Working from home trends today

Now the UK has fully opened up, a majority of employers have embraced new ways of working. As workers demand a better work life balance, Covid WFH practices also demonstrated that businesses could still be just as productive. As we saw with key worker lockdown policies, working from home is more feasible for some types of workers than others. High earners are the ones most likely to be benefiting from a hybrid work environment, with 38% of workers earning £40,000 or more currently working both in the office and at home.

Meanwhile, lower earners are less likely to WFH at all. Lower earners who reported hybrid working between 27 April and 8 May 2022 included:

- 8% of those earning up to £15,000

- 24% of those earning between £15,000 and £20,000

- 21% of those earning between £20,000 and £30,000

- 32% of those earning between £30,000 and £40,000

There also seems to be an age element to those either able to or wanting to WFH, as those aged 30 to 49 most likely to do so.

These changes in working patterns have had a material impact on the housing market. Any further changes or an impending recession will either reverse or accelerate those shifts. Only by understanding the unique data points that create each individual householder can businesses adjust to new trends.

View our Interactive map

Who can afford a home today?

Millennials' homeownership decline

Outra’s data has been featured in the The Spectator on why many people simply cannot afford to become homeowners.The Spectator used our data and found the proportion of millennials buying a home has dropped 11% in five years – a fall in spend of just under £25bn-a-year.The data is yet further evidence of a gaping generational divide in the UK property market and raises concerns that financially hard-pressed millennials are struggling to get on the housing ladder, which is likely to have a significant impact on their financial future given that a house is normally the most valuable thing a person owns.To read the full article - click here

Weathering the Storm of the Cost of Living Crisis

Business survival in economic crisis

The retail, utilities and credit sectors are facing one of the greatest challenges of the past 40 years: As the economic situation worsens, a recession becomes more and more likely. Households feel the pressure and businesses need to adapt to survive. So, what can companies do to weather the storm and thrive during this new challenge?

The perfect storm

In a post-Covid world there were glimmers of growth, but as the world has opened back up, we’ve faced a new wave of challenges. As a result, the UK is seeing a dramatic reduction in spending. On June 24th, the Office of National Statistics (ONS) announced that the volume of goods sold in-store and online in May 2022 fell by 0.5%.

With inflation at its highest level since the 1980s, we’re experiencing all-time lows in consumer confidence. As food and energy prices continue to rise, this trend is likely to continue throughout the summer.

Some of the industries most affected by the crisis are retail, credit, and utility. Each industry faces unique challenges and in turn, will need to deliver a unique strategy in response.

- Retail businesses will need to be smarter at customer targeting and retention to ensure a healthy flow of new shoppers while preventing the loss of existing loyal customers.

- Credit providers must address the increased need for credit along with an increased risk of defaults or fraud.

- Utility companies must improve their processes for supporting vulnerable customers to adhere to regulations, along with a moral duty to support these households.

Data insights and the 2022 consumer

Consumers are adopting more defensive spending behaviours to ensure they have enough money to pay for the essentials. These tactics include self-imposed checkout limits at supermarkets, reducing expenditure on luxuries, or borrowing to fund everything from clothes to food.

The change in consumer behaviour creates a reduction in disposable income for businesses in the affected sectors. With a reduction in income comes a hit to companies’ bottom lines — threatening the survival of many of them. Small businesses are particularly at risk as they lack the cash flow necessary to recover from low-income periods.

Each UK household is unique. For consumer-focused businesses, understanding each of these, whether they are an existing customer or not, will be key to success. By using data that provides detailed insight at an individual post box level, businesses can gain a true understanding of the UK consumer.

Leveraging customer data science and data modelling provides the ability to turn data into wisdom — which in turn, forms the bedrock for any business or marketing strategy through an understanding of the unique nature of each customer, and the unique issues they are facing.

Adapt. Overcome

In the current environment, identifying which UK households are most likely to be affected by the cost of living crisis helps businesses adapt to the needs of their customers. By knowing the financial status of customers at a household level, businesses get a live snapshot of current behaviours. And through modelling that live snapshot, we can then predict customers' future behaviours.

All consumer-facing businesses can use this insight to understand:

- Who are my customers, and how are they dealing with increased living costs?

- What is important to my customers?

- How do I ensure my marketing messaging is effective?

- Who should I target, and what’s the best channel to use to do it?

But this data can also help overcome unique challenges within each sector.

For Retail, this insight can identify which physical store locations might face the most amount of pressure from reduced takings. Those located in the most hard-hit locations are likely to see a reduction in foot traffic and profits. Using data science, retailers can implement strategies ahead of time to address the issue, such as stocking cheaper products, creating targeted promotions or advertisements, or even reducing the number of physical stores.

Credit agencies and lenders can use the data to pinpoint households that are more likely to default. This goes beyond the process of deciding on whether to extend credit or not at the point of sale. It can identify households that already have credit, but now have a propensity to default. To better support those that face financial hardship as well as to manage credit risk.

The same is also the case for Utility providers. The current energy crisis has put an increased regulatory burden on providers. Our analysis has identified 5,055,359 vulnerable households out of the circa 30 million in the UK by modelling features beyond simple financial flags. Each one of those is considered a financially vulnerable household that they are obliged to actively provide additional support.

Data science at a household level can help consumer-facing businesses adapt and overcome the challenges that lay ahead. Through understanding where consumers are at this moment in time, and where they might be in six months, we can identify behaviours and keep your business ahead of the curve.

The Hidden Reality of UK Energy Costs

Understanding UK's energy crisis

As winter begins to set in, the reality of the cost of living crisis is beginning to take hold. While inflation has been affecting the economy as a whole, the increase in UK energy costs has been especially steep. Even with government intervention, energy price hikes will place huge pressure on UK households. In particular, the most vulnerable, those with larger homes, and homes with a lower EPC rating.

The crisis isn’t affecting customers equally. Our data has identified regional variations in household finances and building quality which will mean some homes will face higher costs than others. Consumer facing businesses and regulators need to understand these regional differences at a household level, to not only maintain the bottom line, but to ensure the most vulnerable customers are being supported.

UK faces average energy bills of over £4,000

UK energy costs have increased due to the rising price of wholesale gas across 2021 and 2022. In April, household energy bills increased by 54% and consumers faced a further 80% rise in October.

In response, the UK Government established the Energy Price Guarantee. The programme caps the average unit price for dual fuel customers paying via direct debit from 1st October; 34.0p/kWh for electricity and 10.3p/kWh for gas. This is on top of the £400 Energy Bill Support Scheme.

What is important to note is that this means bills are not capped – they are still based on usage. So, those with larger homes, homes with a lower EPC rating, or those with additional heating needs (such as remote workers) will face bills far in excess of the governments proposed nationwide average.

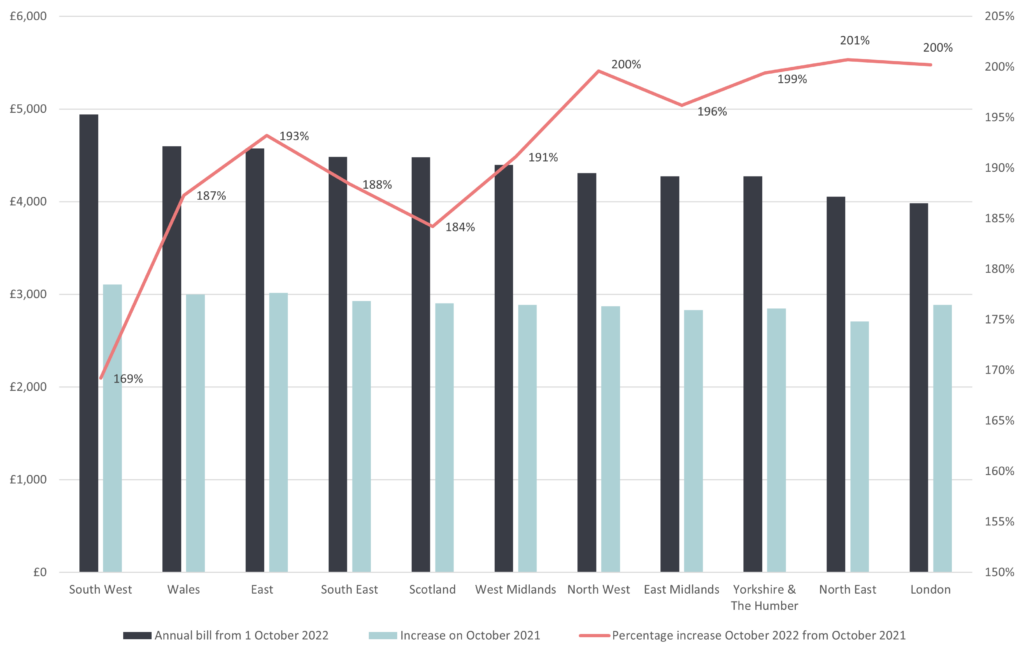

The government has stated that the average household energy bill will be £2,500 per year. But our data has uncovered that due to these factors, the reality is that average UK energy costs will be more than £4,000 - a 150% increase from 2021.

“Across the UK, the minimum year-on-year increase according to our calculations will be 169%, which will result in more consumers having to tighten their belts and reduce their spending elsewhere to afford to pay their bills.”

-

Peter Jackson, Chief Data and Product Officer at Outra

What is the regional reality?

The UK has vast geographical differences, so a single average figure for bills can be extremely misleading. Financial disparity across the UK is nothing unexpected, but the scale at which the cost of living energy crisis will affect different regions could have long-term effects on households. By diving into Outra’s data, we have identified at a household and regional level where the rise will have the greatest impact.

Regional breakdown of UK energy bills from 1 October 2021

The chart demonstrates that while bills will rise to roughly £4,000 on average, some regions will face costs of nearer £5,000. On the other end of the spectrum, while London and the North East have the lowest annual bills, they will endure the largest relative price increases of around 200% each.

The reality of the cost of living crisis will be further exacerbated by the north/south income disparity. Colder areas like Scotland and the North, and more deprived regions in major cities will bear a larger cost burden.

Household data, means regional solutions

In the face of the cost of living crisis, understanding each individual household will be essential for any consumer facing business. It’s clear that national averages do not accurately represent the reality of the UK consumer. By being able to anticipate the economic forces impacting UK customers at a household level presents immense opportunities.

Whether you are looking to support vulnerable customers, retain existing customers when belts are being tighten, or looking to expand into a new customer base, household level data can provide the insights you need to be successful.

Every household is made of up its own unique data points. Each one builds upon the other to create detailed personas of who your existing customers are, and helps to identify new lookalike audiences.

Disposable income is being squeeze, and the reality of the cost of living is yet to set in. Only data driven marketing solutions can help your brand forecast risk, predict churn and deliver personalised messaging. Afterall, we’ve already identified around 5 million vulnerable UK households – do you know where they are?

Find out more about our Vulnerability Index or see how we can help your business

Vulnerability Summit 2023 Round Up

Outra co-sponsors Vulnerability Summit

On the 20th of July, Outra proudly co-sponsored the Collaboration Network’s Vulnerability Summit in conjunction with BSI. The Vulnerability Summit contained a wide range of expert speakers and panellists featuring representatives from the Vulnerability Registration Service, Citizens Advice, Samaritans and many more. Below are some of our teams’ key takeaways from the event.

Single Source of Truth

Many organisations and charities typically rely on their own customer parameters as a source for vulnerability which is not a full-picture approach. An accurate representation of vulnerability uses enhanced and predictive data to deliver unparalleled insights into who a business’s vulnerable consumers are or might be. The latter, ‘might be’ is crucially important here. Layering data and modelling it to identify those ‘at risk’ of vulnerability is the way in which businesses can stay ahead of the curve and predict, pre-empt, and prepare so they can best cater to the needs of those at high risk. Of course, this is especially relevant with the Financial Conduct Authority’s ‘Consumer Duty’ coming into effect this year.

Financial Services

The content of the summit included discussions around the financial services sector and how businesses in this space can best engage with their vulnerable customers. Sentiment showed the goal for the financial services sector is to reach a point where customers feel able and well-informed enough to notify organisations on their need for help and for there to be sufficient infrastructure to deliver this help, almost to a self-regulated degree.

Predictive data

Building on this need for a regulated delivery of help and support, it was felt that organisations should diversify their approach to vulnerability. Using Outra’s predictive Vulnerability Index, organisations can identify vulnerable households and implement the appropriate measures well in advance of when households may decide to ask for help. Predictive data can help identify vulnerable individuals who might be financially excluded due to factors such as low income, lack of credit history, medical reasons, or other barriers. With this knowledge, businesses can operate more inclusively to a broader segment of the population, reducing the risk of financial exclusion and promoting economic well-being.

Leveraging data responsibly creates a more equitable and supportive environment for all consumers, regardless of their vulnerabilities or challenges.

The Power of Change in Segmentation

Utilising change for predictive segmentation

It is often said that the only constant is change. Why, therefore is change rarely used as a variable in segmentation? The purpose of segmentation is to create powerful models that make predictions based upon the data that feed them. For example, the surprise Brexit vote could easily have been predicted if changes in immigration patterns had been analysed before the referendum. The areas in the UK that had experienced a significant net increase in immigration since 2011 were more likely to vote Remain, whilst locations which over the course of six years remained stable in terms of their multi-culturalism voted Leave. In this case change was the predictive variable.

So how can this be applied to marketing?

Very easily. For instance, in the case of consumer credit. Typically, credit providers use scorecards based on huge volumes of demographic and financial behaviour data to determine which customers should be offered extended levels of credit.

But these models, in our experience, are seldom as predictive as they should be. And the reason for this is that they do not use longitudinal transactional data to track changes in the financial situation of customers.

The scorecards tend to feed a single segmentation which is credit worthiness rather than a two-dimensional segmentation which should also contain financial transaction data over periods of time. If change was made the predictive variable more appropriate limits could be offered to customers making the credit industry more responsible.

Over the past 30 years, the trend in the data industry has been for increasingly granular data to be used as the foundations for classification systems, not least because of improved computing power.

As this has happened, the misconception that more detailed data is better than less granular data has manifested itself. However, often this is not the case.

Sometimes the most powerful data is tracking change rather than volume or depth of the data.

So, the question to ask yourself is what changes can you track and would they form the basis of a powerful prediction for your business?

Reflections on my first 100 days at Outra part 3

Outra's rapid agile innovation

In part 1 of my first 100 days reflections I mentioned that things at Outra seem to happen 4x faster, that’s why it isn’t the first 100 days reflection that you expect.

The pace of data engineering, data science, innovation, and sales has astonished me; there is real pace and agility. This is down to three things: the data fabric architecture, the operating model and the people. Yes you’ve got it: Technology, Process and People.

I’ll write elsewhere about the Outra data fabric architecture, and I spoke about it at the A-Team Group Data Management Conference in London recently, so I won’t say much more here beyond the fact that it gives the data science and innovation teams amazing flexibility and capability for agility.

The operating model is fascinating: we have data engineers reporting into the CTO (more elsewhere), Data Scientists reporting into the Chief Data Scientist and the Innovation Team (Explorer team) reporting into me.

The Explorer team are supported by the other two teams and are set up to push the boundaries and develop new products beyond MVP. This is where the exceptional agility is taking place; products being designed and built in hours and days rather than weeks and months. These innovations are then market tested with clients and, if proven, passed back into the other two teams for ‘production’.